Ms. A heard about Housing Upgrades to Benefit Seniors (HUBS) through her church, and she decided it was time to reach out.

“My roof was leaking. There were two sun lights that were also damaged on the roof. I had to put pots and buckets out to catch the rain…And there was no way I could afford to get it fixed.”

According to the National Aging in Place Council, over 90% of seniors say that they would prefer to age in place instead of moving into senior housing, but because older adults are more likely to live on a fixed income and experience limited mobility, they often have substantial housing repair and social support needs.

In Maryland, one in four households with residents 85 years or older and one in five households with residents aged 65-74 pay at least half of their fixed income on housing. In Baltimore City, 17% of all older adults over the age of 65 live below the poverty level.

Concerned for the wellbeing of older Baltimoreans, a coalition of service providers and funders came together to create the Housing Upgrades to Benefit Seniors (HUBS) initiative – a network of organizations with a shared mission of helping older homeowners in Baltimore age in place.

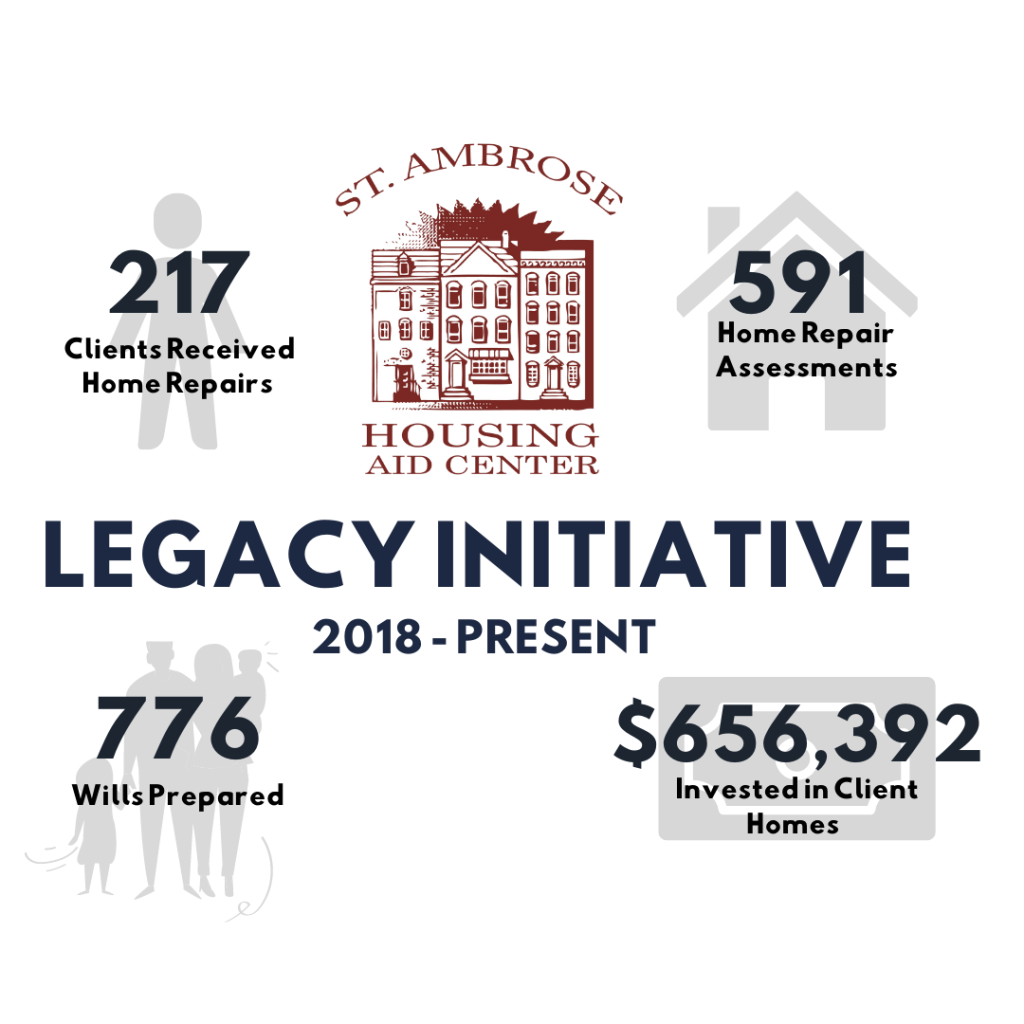

Another partnership, Safe & Healthy Homes, founded in 2021, serves legacy homeowners who have been in their home for ten years or more, as well as homeowners over 65 in Central Baltimore.

Reducing the displacement of both older and legacy homeowners is foundational to strong, healthy, and stable neighborhoods.

Hundreds of older Baltimore neighbors like Ms. A are receiving home repairs and holistic support through service providers including St. Ambrose.

“When you get to a certain age these situations really wear on you. I have peace of mind now, and I didn’t have any peace when my roof was leaking. There has been so much rain lately. I thank God for my new roof.”

St. Ambrose provides not only home repairs, but also will preparation services (to ensure the homes safe passage to heirs) and case management to support older homeowners and legacy homeowners so they can obtain resources like energy assistance and assistance through the Supplemental Nutrition Assistance Program (SNAP).

Comprehensive, holistic services enable homeowners to resolve a variety of issues, including legal issues threatening their housing, issues affecting their ability to afford housing payments, and issues influencing safety and habitability.

These services include home modifications to facilitate safety and health (the installation of stair lifts, grab bars, railings, shower chairs, roof and furnace repair), and legal advice to avoid the threat of foreclosure or the threat of tax sale. They also ensure that the critical asset of the home can stay in the client’s family, helping to stabilize neighborhoods and build intergenerational wealth.

Our older and legacy neighbors do so much to strengthen our communities, and St. Ambrose is honored to be one of many Baltimore organizations coming together to support and invest in our neighbors and in the strength, stability and wellbeing of our communities.

A huge thanks to Ms. A for sharing her home repair experience with us and for Ms. W for sharing the stair lift photo.

Interested in Accessing these Services?

If you or someone you know is 65 or older click here to learn more about eligibility and next steps.

If you or someone you know is a legacy homeowner who has lived in their home for more than ten years or is 65 or older in Central Baltimore click here to learn more about eligibility and next steps.